The Biggest Corporate Tax Cut in U.S. History: How Section 199A of the TCJA Changes Choice of Entity Decisions for Closely-Held Businesses

By Barbara Zanzig Lock

Introduction

How do you advise your business clients on which entity is best for their closely-held business? Because most choices offer the desired limited liability, tax consequences are frequently the deciding factor. Those consequences changed with the 2017 Tax Cuts and Jobs Act (TCJA).[i]

Before the TCJA, the choice-of-entity landscape was fairly settled. Most small businesses chose a pass-through entity,[ii] usually an LLC or an S corporation. Then, with the White House promising a system that “encourages companies to stay in America, grow in America, spend in America, and hire in America,”[iii] Congress passed the TCJA. This act decreased the top corporate tax rate from 35 percent to 21 percent. This was the biggest corporate tax cut in U.S. history.

So why didn’t practitioners advise their clients to immediately start forming C corporations to take advantage of the savings? They might well have, but before the TCJA passed, owners of pass-through entities pushed for a comparable cut for their own businesses. The result was the show-stealing section 199A.[iv] This complex and arbitrary provision allows an unprecedented 20 percent business income deduction for owners of pass-through entities.

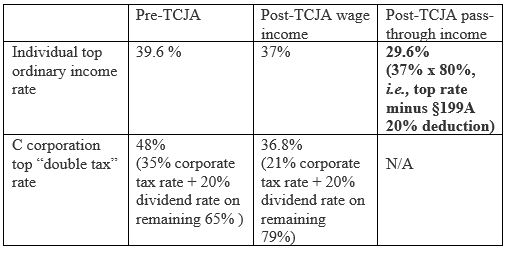

How significant is section 199A? While the TCJA reduced the top individual ordinary income tax rate from 39.6 to 37 percent, the top rate for income eligibility for the section 199A deduction is 29.6 percent. That’s significant. The bottom line: although the TCJA’s hallmark was the C corporation tax rate cut, the action for the closely-held business is in section 199A.

Section 199A: Overview, mechanics, limits

What is the Section 199A deduction? For tax years 2018—2025, any taxpayer other than a corporation or employee, may deduct up to 20 percent of “qualified business income” (QBI)[v] from a “qualified trade or business.”[vi] The deduction is available for income from businesses operated as sole proprietorships, partnerships, LLCs, S corporations, trusts, and estates.

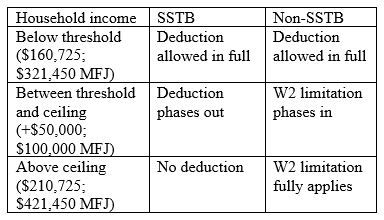

A “qualified trade or business” includes every trade or business other than that of being an employee and certain businesses designated as a “specified service trade or business” (SSTB).[vii] A taxpayer may deduct income from an SSTB, but the deduction phases out once the taxpayer’s household income exceeds a threshold amount.[viii] This SSTB limit and the exclusion of wage income from the deduction are intended to restrict the deduction to business rather than personal service income.

Section 199A and the final regulations provide a list of businesses they characterize as SSTBs. Architecture and engineering were omitted from the list of SSTBs. In addition, there is a de minimis exception to SSTB classification for a business with gross receipts less than $25 million.[ix] Such business is not an SSTB if 10 percent or less of its gross receipts are attributable to services performed in a disqualified field.

Businesses Characterized as SSTBs

- Health

- Law

- Accounting

- Actuarial science

- Performing arts

- Consulting

- Athletics

- Financial services

- Brokerage services

- Investing and investment management

- Trading

- Dealing in securities, partnership interests, or commodities

- Any trade or business where the principal asset is the reputation or skill of one or more of its employees.

Not surprisingly, the SSTB has proven difficult to define. For example, the brokerage services category includes stockbrokers, but not real estate and insurance brokers.[x] Investment management does not include real estate management.[xi] Financial services includes investment banking and retirement advising, but not taking deposits or making loans.[xii] What if a bank offers investment banking services? Is the bank an SSTB?

A second restriction on the deduction phases in as the taxpayer’s household income exceeds a threshold amount. This income threshold is the same as that for the SSTB limitation.[xiii] The second restriction limits the taxpayer’s deduction based either on W2 wages the business pays or on a combination of W2 wages paid and the original cost of the business’s depreciable property.[xiv] The depreciable property limit was added to appease rental property owners, who often pay management fees rather than wages. It allows them to take advantage of the deduction without rearranging their businesses.

Because the deduction has limits based on the taxpayer’s household income, taxpayers take it on their form 1040. It is a below-the-line deduction available in addition to the standard deduction or itemized deductions. [xv]

So how does the deduction work? Let’s start with a basic scenario, where section 199A’s application is fairly straightforward. Assume Jane is a single attorney with a solo practice. She earns $150,000 from her law practice, and this is her only income. Jane may deduct 20 percent of her QBI, or $30,000. Although Jane’s business is an SSTB, her deduction is not subject to the SSTB limit or to the W2 wage limitation because her household income does not exceed the threshold amount, which is $160,725 in 2019 ($321,450 for married filing jointly (MFJ)).[xvi]

Now let’s add a complicating factor. Jane is married to Hank, who earns wages of $300,000 working as a physician employed by a hospital. Hank does not qualify for a section 199A deduction, because wages are not QBI. But his wages count toward household income, affecting Jane’s entitlement to a Section 199A deduction. The couple’s household income is $450,000, which exceeds the phase-out ceiling. Because Jane works as an attorney, which is an SSTB, she loses her section 199A deduction.

Now let’s add one more twist. Suppose Hank still earns $300,000 wages, but Jane makes $150,000 as a self-employed real estate broker instead of an attorney. The couple’s household income still exceeds the threshold, but Jane’s business is not an SSTB. So is Jane entitled to a Section 199A deduction? It depends. If Jane’s business has no depreciable assets, Jane’s deduction is limited to 50 percent of the W2 wages the business pays employees. If she pays her assistant $30,000 in 2019, Jane may take a $15,000 section 199A deduction.

Maximizing the Section 199A Deduction

What to do with all of this? This article cannot give more than a superficial overview of the section 199A deduction. But here are a few things to take away.

The deduction gets very complicated very quickly. Consider that Congress recently released a 274-page document containing both final regulations explaining section 199A and explanations of those final regulations. But, despite its complexity, any practitioner advising a client about business formation should still be aware of its existence and potential impact.

The deduction offers incentives to reevaluate. Section 199A creates an incentive to run otherwise non-business income through a business to qualify for the deduction. For example, suppose Frank’s hobby is refurbishing guitars and selling them on eBay. If he sells enough guitars, and he sells them consistently enough, his hobby may rise to the level of business and he may qualify for the 20 percent deduction. But section 199A and its regulations do not define trade or business and, in fact, Treasury and IRS declined requests for a bright-line test in the final regulations. The definition of trade or business for tax law remains a facts and circumstances one based on the taxpayer’s profit motive and level of activity.[xvii]

The deduction also encourages employees to become independent contractors. Of course, independent contractor status has its disadvantages, such as increased payroll taxes and the loss of employment benefits, but section 199A changes the equation by creating a 20 percent deduction for the independent contractor.

The deduction poses traps for the unwary. Suppose Jim owns a small plumbing business as an LLC. Jim has no employees, does all the plumbing work himself, and earns $150,000 in 2019 from his labor. Jim’s wife, Kate, earns $300,000. Ignoring the depreciable asset limit, Jim’s section 199A deduction will be $0. Why? Jim’s household income is above the ceiling amount and he pays no W2 wages—an LLC member’s compensation is not W2 income. How can Jim remedy this result? He can “check the box”[xviii] to have the LLC taxed as an S corporation, in which case Jim’s compensation will count as W2 income.

Or suppose instead Jim’s partner is Julia, a famous chef, and their business consists of a restaurant and adjacent shop that sells cookware and utensils bearing the chef’s name. Jim manages both the restaurant and the shop. Is the business’s principal asset Julia’s skill or reputation, making it an SSTB for all owners, including Jim?

The final regulations say the skill or reputation limitation applies only to fact patterns where one receives compensation for appearances, for endorsing products or services, or for licensing the person’s identity.[xix] According to the final regulations, Julia has two businesses: one is being a chef and owning restaurants, which is not an SSTB, and the other is the business of receiving endorsement income, which is an SSTB.[xx] Query what this means for Jim, Julia’s minority partner?

And what about consulting businesses? They are section 199A SSTBs. But don’t virtually all businesses involve consulting? According to the final regulations, consulting means providing professional advice and counsel, but not training and educational courses, to clients. It also does not include providing consulting services ancillary to the sale of goods or performance of services on behalf of an otherwise non-SSTB, such as typical services provided by a building contractor, if there is no separate payment for the consulting services.[xxi] Such distinctions promise to be difficult, if not impossible, to apply consistently.

The deduction does not treat all pass-through entities alike. In theory, it does. But, in practice, a business owner with less than the threshold household income might be better off as an LLC or sole proprietor, while one with income exceeding the threshold might be better off as an S corporation. Why? Assume two single-owner businesses each earn $100,000 net business income and distribute $80,000 to their respective owners as compensation for services. The LLC’s entire $100,000 is QBI potentially eligible for the section 199A deduction. But the S corporation must pay its shareholder-employee a reasonable salary, and that reasonable salary is not QBI. Assuming the $80,000 is the shareholder’s reasonable salary, the S corporation will have only $20,000 of QBI.

Now suppose the businesses each earn $300,000, and each distributes $200,000 to its owner as compensation. The LLC has no section 199A deduction because it pays no W2 wages.[xxii] An LLC owner’s compensation is by definition not W2 income.[xxiii] The S corporation, on the other hand, has paid $200,000 in W2 wages. The shareholder’s potential section 199A deduction is $100,000, or 50 percent of the W2 wages paid, assuming the $300,000 qualifies as reasonable compensation.

S corporations still maintain the self-employment tax savings advantage over LLCs and other pass-through entities. Now that advantage can be combined with the section 199A deduction.

An S corporation’s earnings exceeding the reasonable salaries it must pay its shareholder-employees are not subject to self-employment tax.[xxiv] This quirk gives the S corporation a tremendous tax advantage over the LLC, where every dollar earned is self-employment income. But, as we just saw, S corporation shareholder salaries are not Section 199A QBI, so they reduce the corporation’s deductible income, thereby reducing the deduction itself.

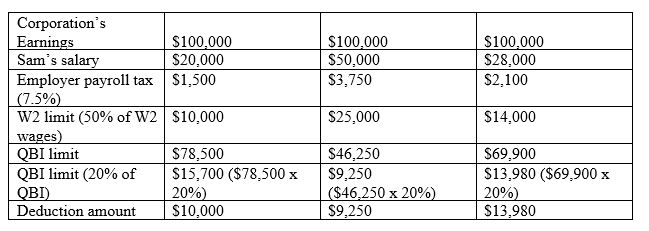

So how can an S corporation achieve Pareto optimality, maximizing its section 199A deduction while sacrificing as little self-employment tax savings as possible? Not surprisingly, this question has been asked and answered. When the corporation pays approximately 28 percent of its income in salaries—which may or may not be reasonable—it optimizes the combination of section 199A deduction and self-employment tax savings.

If it pays more in salary, the shareholders forfeit their self-employment tax savings and pay too much in Medicare and Social Security. If it pays less in salary, the shareholders forfeit section 199A deduction because of the too-low W2 wages cap. The optimal point is where those limits equal each other, which is when salaries are approximately 28 percent of earnings.

Consider, for example, Sam, the sole shareholder whose S corporation earns $100,000, but whose household income makes him subject to W2 limits. If the corporation pays Sam a $20,000 salary, assuming 7.5 percent employer payroll tax, Sam has a potential $15,700 deduction, but the W2 limit caps his deduction at $10,000. At a $50,000 salary, the W2 cap is $25,000 but his deduction is limited to $9,250, or 20 percent of income. Finally, when his salary is 28 percent, his potential $14,000 deduction is capped at $13,980. The deduction is maximized.

The deduction offers planning opportunities: Section 199A encourages “cracking” and “packing,” i.e., strategies that qualify an SSTB’s income for the deduction.[xxv] For example, a law firm, which is an SSTB, buys its office building through an LLC. The LLC rents the office to the law firm, which deducts the rental payments as a business expense. Can the lessor entity qualify for the section 199A deduction? The final regulations say no if the businesses share 50 percent or more common ownership. But what if they don’t? There is plenty of room for planning to maximize the section 199A benefit.

Conclusion. While the TCJA added a significant player to the team in the form of section 199A— one which business lawyers should be aware of— it did not change the winner of the game. The TCJA effectively retained the tax advantage for pass-through entities, particularly S corporations, while adding some tax-saving opportunities and potential traps. Section 199A’s unprecedented business income deduction, together with its complexity and sheer arbitrariness, make it worth some study. The bottom line is, entity choice still requires a facts and circumstances analysis of your client’s particular situation, but section 199A is now likely to be a major part of that analysis.

Barbara Zanzig Lock is an associate clinical professor and director of the federal income tax clinic at the University of Idaho College of Law in Boise. She has taught for the College of Law since it welcomes its first Boise third-year class in 2010. She teaches federal income tax and wills, trusts, and estates.

[i] Pub. L. No. 115-97.

[ii] A pass-through entity is not a separate taxpayer. Rather, it passes its income through to its owners, and the income is taxed only at the owner level. Examples of pass-through entities are sole proprietorships, partnerships, LLCs, and S corporations. In contrast, a C corporation is a separate taxpayer from its owners. Corporate income is taxed to the corporation when earned, and then again to the shareholders when distributed.

[iii] https://www.whitehouse.gov/briefings-statements/remarks-president-trump-tax-reform/.

[iv] 26 U.S.C. §199A.

[v] QBI is the net amount of qualified items of income, gain, deduction, and loss with respect to a qualified trade or business. 26 U.S.C. §199A(c).

[vi] 26 U.S.C. §199A(c)(1). Section 199A does not define trade or business. But, solely for the purposes of § 199A, a safe harbor exists for individuals and pass-through entity owners with respect to a rental real estate enterprise. See IRS Notice 2019-07. Rental real estate that does not meet the requirements of the safe harbor may still be treated as a trade or business for purposes of the QBI deduction if it qualifies as a §162 trade or business.

[vii] 26 U.S.C. § 199A(d)(2), referencing 26 U.S.C. §1202(e)(3)(A).

[viii] 26 U.S.C. § 199A(d)(3)(B).

[ix] 26 C.F.R. § 1.199A-5(c)(1).

[x] 26 C.F.R. § 1.199A-5(b)(2)(x).

[xi] 26 C.F.R. § 1.199A-5(b)(2)(xi).

[xii] 26 C.F.R. § 1.199A-5(b)(2)(ix).

[xiii] 26 U.S.C. § 199A(b)(3)(B).

[xiv] Sec. 199A(b)(2)(B)(i) & (ii). Above the income ceiling, the QBI deduction for a non-SSTB is limited to the greater of the taxpayer’s share of 50% of W-2 wages paid to employees during the tax year and properly allocable to QBI, or the sum of the individual’s share of 25% of such W-2 wages plus the individual’s share of 2.5% of the unadjusted basis immediately upon acquisition (UBIA) of qualified property, usually its original cost. Qualified property means depreciable tangible personal property.

[xv] To prevent taxpayers from taking the §199A deduction for income already taxed at preferential rates, the deduction is further limited to the amount by which the taxpayer’s QBI exceeds net capital gain for the year. §199A(a)(2), (b)(1), (2).

[xvi] §199A, Rev. Proc. 2018-57.

[xvii] In Commissioner v. Groetzinger, 480 U.S. 23 (1987), the Supreme Court stated, “[w]e conclude that if one’s gambling activity is pursued full time, in good faith, and with regularity, to the production of income for a livelihood, and is not a mere hobby, it is a trade or business within the statutes with which we are here concerned.”

[xviii] 26 CFR § 301.7701-3. The “check the box” regulations permit certain business entities to choose their classification for U.S. federal income tax purposes by checking the box.

[xix] 26 C.F.R. § 1.199A-5(b)(2)(xiv).

[xx] 26 C.F.R. §1.199A-5(b)(3), ex. 15.

[xxi] 26 C.F.R. §1.199A-5(b)(2)(vii).

[xxii] This example, again, ignores the depreciable assets (UBIA) portion of the W2 wages test.

[xxiii] In Rev. Rul. 69-184, 1969-1 C.B. 256, the IRS classified partners as independent contractors rather than employees.

[xxiv] In Rev. Rul. 59-221, 1959-1 C.B. 225, the IRS rules that S shareholders’ distributive shares are not subject to self-employment tax. To prevent abuse of this rule, the IRS requires S corporations to pay reasonable compensation to shareholder-employees.

[xxv] For more on cracking and packing, see David Kamin et al., The Games They Will Play: Tax Games, Roadblocks, and Glitches Under the 2017 Tax Legislation, 103 Minn L. Rev. 1439 (2018).