Planning for Death, Brought to Life: Thoughts from a Professional Fiduciary by David C. Cooper

“…Texas authorities searched yesterday for the bodies of two of four people swept into the Pedernales River when they tried to cross on steppingstones. Two bodies were recovered Sunday.”[1]

by David C. Cooper

Why Do I Work as a Professional Fiduciary?

For most of my career, I have worked as a professional fiduciary in the context of trust and estate administration.

I was likely drawn to this area of practice based on personal experience at a young age. The newspaper article quotation above refers to my parents, oldest brother, and sister who perished in a drowning accident while I was in high school. At the time of the accident my father, George, was academic dean at the junior college in my hometown, and my mother, Wilma, taught sixth grade. Along with my sister, Leslie, we were visiting our oldest brother, Guy Cooper, who had just completed his first year of law school at the University of Texas. Our brother, Kevin, was not with us on the trip.

As teachers of modest financial standing, my parents were unlikely candidates to have created a trust at their passing. That said, life insurance proceeds funded a trust that protected assets for surviving children through age 21. My dad’s brother, Victor, served as trustee. Uncle Vic was a Baptist minister and WWII veteran – not a financial or legal professional. However, his caring service as trustee provided a solid foundation from which I was able to advance my education and professional career.

Throughout this article, I’ve included quotations in an attempt to add color to the specific topic being discussed. The following may describe how I felt after my family’s accident:

“I was bruised and battered

I couldn’t tell what I felt

I was unrecognizable to myself…”

Bruce Springsteen[2]

Perhaps our clients experience similar feelings after a significant loss.

What Is a Professional Fiduciary?

“Walk a mile in my shoes…”

Joe South[3]

A simple understanding of fiduciary might be to “walk in someone else’s shoes,” i.e., represent someone who is unable to represent themself.

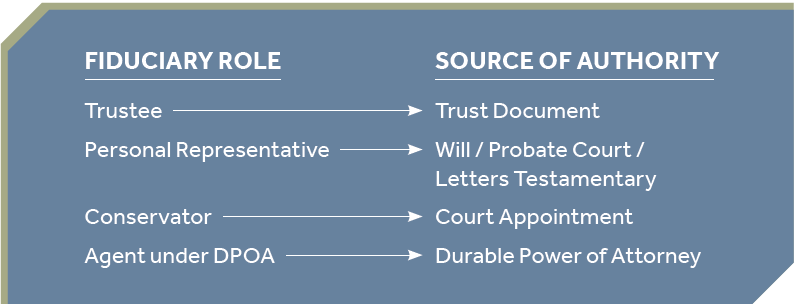

The primary fiduciary roles I have engaged in include trustee, personal representative, conservator, and agent. Fiduciaries serve a very important function in the end-of-life spectrum of needs, which of course also includes estate planning and elder law attorneys, caregivers, and others. As a fiduciary, I am at the back end of the estate planning process, typically called on to serve when someone has passed away or experienced a situation of incompetency.

Core responsibilities of a professional fiduciary include understanding and integrating relevant law, property issues, and working with people.

The following are perspectives I have developed over the past 25 years as a professional fiduciary.

Consider Starting Basic When Describing the Roles of a Fiduciary

As noted, “fiduciary” is a broad term describing standing in the shoes of another person or entity, with the obligation to put the best interests of the other person or entity ahead of those of the fiduciary. Idaho Code § 63-3007 provides a statutory definition.[4]

The following is a very fundamental description of fiduciary roles. I typically receive positive feedback when I cover this with prospective clients.

/*! elementor – v3.21.0 – 26-05-2024 */

.elementor-widget-image{text-align:center}.elementor-widget-image a{display:inline-block}.elementor-widget-image a img[src$=”.svg”]{width:48px}.elementor-widget-image img{vertical-align:middle;display:inline-block}

Consider the Spectrum: An Estate Plan Is Only as Good as Its Implementation

“For all its uncertainty, we cannot flee the future.”

Barbara Jordan[v]

Creating an estate plan is only the beginning. Due consideration must also be given to investing in the administration, execution, and implementation of the plan.

The well-drafted estate plan is an investment that deserves to be implemented by a responsible individual (typically with ample professional assistance), or a professional fiduciary. While it is difficult to know which individuals will survive us and be willing to serve, it is not my contention that every plan needs a professional fiduciary. The able service of my Uncle Vic serves a great example of who an individual trustee may work successfully. That said, it is also an accurate observation that a professional fiduciary’s most consistent source of current business opportunities are trusts and estates where individuals were named as fiduciaries, and where neglect, errors, or malfeasance have occurred.

Where legal disputes arise between family members, the role of the independent fiduciary takes on even greater importance. Having the assets under the control of an independent third party allows interested parties to sort out legal disputes and/or vent long-held conflict without experiencing insecurity as to asset dissipation.

Retaining a Professional Fiduciary Should Be Viewed as a Risk-Transfer Decision

“Only put off until tomorrow what you are willing to die having left undone.”

Pablo Picasso[vi]

Think for a moment about all the types of insurance we pay for: homeowners, health, auto, malpractice, life, disability, long-term care, etc. Why do we invest in insurance?

Insurance is of course synonymous with “risk transfer.” The fundamental structure of insurance involves realizing a known loss – payment of a premium – to protect against the risk or possibility of a much larger loss. In the context of estate planning and administration, we don’t just seek to protect a large asset in the estate, we strive to protect the entire estate, as well as the specific disposition of trust or estate assets. Further, an efficient and accurate administration of a trust or estate can promote the goal of preserving family relationships.

Engaging the correct individual or professional fiduciary increases the likelihood of achieving all the goals of the well-crafted estate plan. As such, it is appropriate to view this as a straightforward risk transfer decision.

/*! elementor-pro – v3.21.0 – 20-05-2024 */

@charset “UTF-8″;.entry-content blockquote.elementor-blockquote:not(.alignright):not(.alignleft),.entry-summary blockquote.elementor-blockquote{margin-right:0;margin-left:0}.elementor-widget-blockquote blockquote{margin:0;padding:0;outline:0;font-size:100%;vertical-align:baseline;background:transparent;quotes:none;border:0;font-style:normal;color:#3f444b}.elementor-widget-blockquote blockquote .e-q-footer:after,.elementor-widget-blockquote blockquote .e-q-footer:before,.elementor-widget-blockquote blockquote:after,.elementor-widget-blockquote blockquote:before,.elementor-widget-blockquote blockquote cite:after,.elementor-widget-blockquote blockquote cite:before{content:none}.elementor-blockquote{transition:.3s}.elementor-blockquote__author,.elementor-blockquote__content{margin-bottom:0;font-style:normal}.elementor-blockquote__author{font-weight:700}.elementor-blockquote .e-q-footer{margin-top:12px;display:flex;justify-content:space-between}.elementor-blockquote__tweet-button{display:flex;transition:.3s;color:#1da1f2;align-self:flex-end;line-height:1;position:relative;width:-moz-max-content;width:max-content}.elementor-blockquote__tweet-button:hover{color:#0967a0}.elementor-blockquote__tweet-button span{font-weight:600}.elementor-blockquote__tweet-button i,.elementor-blockquote__tweet-button span{vertical-align:middle}.elementor-blockquote__tweet-button i+span,.elementor-blockquote__tweet-button svg+span{margin-inline-start:.5em}.elementor-blockquote__tweet-button svg{fill:#1da1f2;height:1em;width:1em}.elementor-blockquote__tweet-label{white-space:pre-wrap}.elementor-blockquote–button-skin-bubble .elementor-blockquote__tweet-button,.elementor-blockquote–button-skin-classic .elementor-blockquote__tweet-button{padding:.7em 1.2em;border-radius:100em;background-color:#1da1f2;color:#fff;font-size:15px}.elementor-blockquote–button-skin-bubble .elementor-blockquote__tweet-button:hover,.elementor-blockquote–button-skin-classic .elementor-blockquote__tweet-button:hover{background-color:#0967a0;color:#fff}.elementor-blockquote–button-skin-bubble .elementor-blockquote__tweet-button:hover:before,.elementor-blockquote–button-skin-classic .elementor-blockquote__tweet-button:hover:before{border-inline-end-color:#0967a0}.elementor-blockquote–button-skin-bubble .elementor-blockquote__tweet-button svg,.elementor-blockquote–button-skin-classic .elementor-blockquote__tweet-button svg{fill:#fff;height:1em;width:1em}.elementor-blockquote–button-skin-bubble.elementor-blockquote–button-view-icon .elementor-blockquote__tweet-button,.elementor-blockquote–button-skin-classic.elementor-blockquote–button-view-icon .elementor-blockquote__tweet-button{padding:0;width:2em;height:2em}.elementor-blockquote–button-skin-bubble.elementor-blockquote–button-view-icon .elementor-blockquote__tweet-button i,.elementor-blockquote–button-skin-classic.elementor-blockquote–button-view-icon .elementor-blockquote__tweet-button i{position:absolute;left:50%;top:50%;transform:translate(-50%,-50%)}.elementor-blockquote–button-skin-bubble .elementor-blockquote__tweet-button:before{content:””;border:.5em solid transparent;border-inline-end-color:#1da1f2;position:absolute;left:-.8em;top:50%;transform:translateY(-50%) scaleY(.65);transition:.3s}.elementor-blockquote–button-skin-bubble.elementor-blockquote–align-left .elementor-blockquote__tweet-button:before{right:auto;left:-.8em;border-right-color:#1da1f2;border-left-color:transparent}.elementor-blockquote–button-skin-bubble.elementor-blockquote–align-left .elementor-blockquote__tweet-button:hover:before{border-right-color:#0967a0}.elementor-blockquote–button-skin-bubble.elementor-blockquote–align-right .elementor-blockquote__tweet-button:before{left:auto;right:-.8em;border-right-color:transparent;border-left-color:#1da1f2}.elementor-blockquote–button-skin-bubble.elementor-blockquote–align-right .elementor-blockquote__tweet-button:hover:before{border-left-color:#0967a0}.elementor-blockquote–skin-boxed .elementor-blockquote{background-color:#f9fafa;padding:30px}.elementor-blockquote–skin-border .elementor-blockquote{border-color:#f9fafa;border-style:solid;border-inline-start-width:7px;padding-inline-start:20px}.elementor-blockquote–skin-quotation .elementor-blockquote:before{content:”“”;font-size:100px;color:#f9fafa;font-family:Times New Roman,Times,serif;font-weight:900;line-height:1;display:block;height:.6em}.elementor-blockquote–skin-quotation .elementor-blockquote__content{margin-top:15px}.elementor-blockquote–align-left .elementor-blockquote__content{text-align:left}.elementor-blockquote–align-left .elementor-blockquote .e-q-footer{flex-direction:row}.elementor-blockquote–align-right .elementor-blockquote__content{text-align:right}.elementor-blockquote–align-right .elementor-blockquote .e-q-footer{flex-direction:row-reverse}.elementor-blockquote–align-center .elementor-blockquote{text-align:center}.elementor-blockquote–align-center .elementor-blockquote .e-q-footer,.elementor-blockquote–align-center .elementor-blockquote__author{display:block}.elementor-blockquote–align-center .elementor-blockquote__tweet-button{margin-right:auto;margin-left:auto}

A professionally crafted plan deserves care

and effective administration.

Fiduciary-Related Expenses Will Arise Whether a Professional or an Individual Is Serving as the Fiduciary

“Beware of little expenses. A small leak will sink a great ship.”

Benjamin Franklin[vii]

Because the duties of a fiduciary are so broad, it is almost inevitable that professional fees will be involved, even if a family member is willing to serve. Stand-alone investment management fees vary, but a reasonable estimate is 1% annual fees – just for management of financial securities. The individual serving as trustee will typically (and wisely) rely on legal advice in fulfillment of fiduciary duties. Further, expenses for retention of tax preparers, property managers, and other professionals, all may come into play.

Professional Fiduciaries with Limited Services Offerings

“Let our advance worrying become advance thinking and planning.”

Winston Churchill[viii]

Serving as a professional fiduciary is a challenging field involving multiple disciplines. Required areas of expertise include but are not limited to communication and people skills, administration, asset management (financial securities, real estate, entities, receivables, etc.), risk mitigation, taxation, operations, financial planning, marketing, and management.

The Limited Services Offering Fiduciary (“LSO Fiduciary”) represents a business model focused on providing only a portion of these services. In the LSO Fiduciary model, fundamental fiduciary duties may be shared with third parties, or outsourced entirely. In the right circumstance, there are attractive attributes to the LSO Fiduciary model, as (for example) it can allow a trusted investment advisor to continue to serve as the primary point of contact for family members.

The LSO Fiduciary model can present the perceived path of least resistance for estate planners and family members in what can be a difficult decision-making process.

The positive attributes come at a cost. For instance, these costs may be associated with conflicts of interest that may arise. The LSO Fiduciary’s ability to select an outside investment advisor creates a marketing opportunity – for the LSO Fiduciary. Close monitoring is important to evaluate whether the third party selected for investment management (or other outsourced services) by the LSO Fiduciary is the best choice for the trust or estate, or the best choice for the LSO Fiduciary.

An additional conflict of interest surfaces when the LSO fiduciary is introduced to the relationship by the investment advisor. The fundamental trustee duty of objectivity is at risk when the fiduciary is beholden to the investment advisor for a particular business opportunity.

Another potential cost comes from the overlay of fees. As noted previously, the outside investment advisor may charge 1% or more. Adding fiduciary fees for administration – which often include a billable hour component in the LSO Fiduciary model – can drive total fees significantly higher.

Next, the outsourcing of custody may present additional costs. An LSO Fiduciary may rely on a third party to have custody of financial securities. As such, assets will not be in direct control of the fiduciary. Outsourcing custody of fiduciary assets may lead to delays in cash movement, and delays in providing accurate accounting for assets.

A final word of caution: LSO Fiduciaries may lack basic expertise in investment management. Lack of investment management expertise at the fiduciary level leaves assets at risk of idle management and could lead to inconsistent supervision of outside managers.

The Intangibles of Tangible Personal Property Disposition

“Twice as much ain’t twice as good

And can’t sustain like one half could

It’s wanting more that’s gonna bring me to my knees…”

John Mayer[ix]

Many of us may feel the gravity of being weighed down by “stuff” – more formally known as Tangible Personal Property (“TPP”). TPP is property that can be touched, used, or consumed, and has intrinsic value. Examples include clothing, vehicles, jewelry, business equipment, furniture, art, silverware, musical instruments, and books.

Disposition of TPP is typically addressed in an estate plan by reference to a writing separate from the will. Per I.C. § 15-2-513, “the writing must either be in the handwriting of the testator or be signed by him and must describe the items and the devisees with reasonable certainty.”[x]

In my experience, less than half of estate plans to be administered include a completed list for disposition of TPP. In post-death administration, it is not unusual to hear from family members that the decedent verbally promised them specific items of TPP. But if it isn’t written down, it typically doesn’t happen.

When an estate owns personal property of significant financial or emotional value, I encourage estate planning attorneys to assist their client in completing the disposition list for TPP. This can be a tremendous service to the family. For example, one memorable list was 115 pages long. This list was typed, signed, and included photographs as well as a brief description of each item and identified its intended recipient. This saved the family significant heartache and disputes, as the decedent had a habit of verbally promising the same items to multiple family members.

Given the potential emotional impact of disposition of TPP, this area is ripe for litigation. Family members may be more willing to fight for grandma’s wedding ring, or granddad’s vintage Martin guitar – so plan accordingly.

Managing Real Estate as a Fiduciary Is Not a Passive Endeavor

“Real estate is a contact sport.”

Tracey Hampson[xi]

It is inevitable that real estate will be a component – perhaps the primary asset – of many fiduciary accounts. This said, it is important to follow a discipline when onboarding and managing real estate.

The “Big 3” steps to be followed include inspection, valuation, and insurance.

The inspection may reveal structural imperfections that need to be addressed, but most importantly should be targeted to health and safety concerns. Recently a trust I was administering owned a house on the Boise Bench that as fiduciary we were preparing to sell. The professional inspection revealed many deficiencies, but most worrisome was an exposed wire in the basement. Cost-wise it was an inexpensive fix for an issue that (left unresolved) could have had disastrous consequences.

The next step to follow is valuation, which may include an appraisal. A fundamental fiduciary obligation is to account to interested parties. Defensible information as to valuation may be best obtained via an appraisal.

Finally, it is essential that adequate insurance coverage be maintained on fiduciary-owned properties. Clients are well-served to work with a professional fiduciary that offers a blanket policy for fiduciary-owned assets across all accounts. In the absence of a blanket policy, a professional fiduciary must maintain contact with multiple agents, track claims quality of multiple carriers, and deal with a multitude of different policy provisions, coverage limitations, and premium due dates.

Serving as a professional fiduciary is a challenging field involving multiple disciplines.

The Financial Strength of a Professional Fiduciary Is Important

“Will you still love me, tomorrow?”

Carole King[xii]

The financial strength of a professional fiduciary is important. A successor fiduciary named in estate planning documents today may not serve for many years, or even decades. Does the professional fiduciary have diverse sources of revenue? Do they report financial information that can be reviewed by the public, such as bank call reports?[xiii] If a private fiduciary will not disclose financial information, how do you know they will be around when needed?

Consider reviewing public information about a professional fiduciary’s financial strength, when evaluating the best fit for your clients.

Conclusion: Plan for the Full Spectrum

“I’d love to change the world

But I don’t know what to do

So I’ll leave it up to you.”

Alvin Lee[xiv]

A message I consistently give to the trust officers on my team is that because the job responsibilities for being a fiduciary are so broad, there are many ways to be a great trust officer. Reviewing my own experience, Uncle Vic had only a modest financial and legal background, but was off the charts in terms of empathy, relatability, and compassion. While a professional fiduciary must possess technical expertise, we often find that the “human” elements are crucial to making an estate plan work. The best fiduciary likely offers a balance of technical expertise and people skills.

Clients are counting on their estate planning attorney for thorough advice, not just a transaction. A professionally crafted plan deserves care and effective administration. Because an estate plan is only as good as its administration and implementation, I encourage you to complete the estate planning spectrum by helping your clients choose the right fiduciary for their circumstances.

/*! elementor – v3.21.0 – 26-05-2024 */

.elementor-widget-image-box .elementor-image-box-content{width:100%}@media (min-width:768px){.elementor-widget-image-box.elementor-position-left .elementor-image-box-wrapper,.elementor-widget-image-box.elementor-position-right .elementor-image-box-wrapper{display:flex}.elementor-widget-image-box.elementor-position-right .elementor-image-box-wrapper{text-align:end;flex-direction:row-reverse}.elementor-widget-image-box.elementor-position-left .elementor-image-box-wrapper{text-align:start;flex-direction:row}.elementor-widget-image-box.elementor-position-top .elementor-image-box-img{margin:auto}.elementor-widget-image-box.elementor-vertical-align-top .elementor-image-box-wrapper{align-items:flex-start}.elementor-widget-image-box.elementor-vertical-align-middle .elementor-image-box-wrapper{align-items:center}.elementor-widget-image-box.elementor-vertical-align-bottom .elementor-image-box-wrapper{align-items:flex-end}}@media (max-width:767px){.elementor-widget-image-box .elementor-image-box-img{margin-left:auto!important;margin-right:auto!important;margin-bottom:15px}}.elementor-widget-image-box .elementor-image-box-img{display:inline-block}.elementor-widget-image-box .elementor-image-box-title a{color:inherit}.elementor-widget-image-box .elementor-image-box-wrapper{text-align:center}.elementor-widget-image-box .elementor-image-box-description{margin:0}

David C. Cooper

David Cooper serves as Chief of Trust and Investment Administration for Idaho Trust Bank. David is based in Boise and manages a team of trust officers and administrators in Boise and Coeur d’Alene. David also works directly with current and prospective fiduciary clients of the bank, and serves as a primary point of contact when attorneys refer prospective clients to Idaho Trust.

David is an Idaho attorney who previously served as President and Bar Commissioner of the Idaho State Bar, and is immediate Past-Chairperson for the Taxation, Probate & Trust Law Section. He has also served as President of the Boise Estate Planning Council and as President of the Treasure Valley Estate Planning Council. He is a member of the Alaska and Kansas Bar Associations and is a graduate of the University of Kansas School of Law and the University of Kansas School of Business. He holds the designations of Certified Financial Planner and Certified Trust & Financial Advisor. In 2022 David was elected as a Fiduciary Counsel Fellow of the American College of Trust and Estate Counsel.

[1] Middle West and East Hit by Rains and Tornados, The New York Times (June 16, 1981).

[2] Bruce Springsteen, Streets of Philadelphia on Philadelphia: Music from the Motion Picture (Epic Soundtrax 1993).

[3] Joe South, Walk a Mile in My Shoes on Don’t It Make You Want To Go Home (Capitol Records 1970).

[4] Idaho Code § 63-3007 (“The term ‘fiduciary’ means a guardian, trustee, executor, administrator, receiver, conservator, or any person acting in a position of trust or fiduciary capacity for any other person or group of persons.”).

[v] American Rhetoric: Barbara Jordan – 1976 Democratic National Convention Keynote Address, https://www.americanrhetoric.com/speeches/barbarajordan1976dnc.html (last visited May 22, 2024).

[vi] Pablo Picasso Quotes, BRAINYQUOTE, https://www.brainyquote.com/quotes/pablo_picasso_120938 (last visited May 10, 2024).

[vii] See Benjamin Franklin, Poor Richard’s Almanac (1732).

[viii] Winston Churchill Quotes, BrainyQuote, https://www.brainyquote.com/quotes/winston_churchill_156920 (last visited May 10, 2024).

[ix] John Mayer, Gravity on Continuum (Sony BMG Colombia Aware 2006).

[x] Idaho Code § 15-2-513.

[xi] Alex Velikiy, 20 Funny Real Estate Quotes, Rontar (Jan. 17, 2024), https://www.rontar.com/blog/funny-real-estate-quotes/ (last visited May 10, 2024).

[xii] Carole King, Will You Love Me Tomorrow on Tonight’s the Night (Scepter 1960).

[xiii] See Federal Financial Institutions Examination Council Central Data Repository’s Public Data Distribution, Federal Financial Institutions Examination Council, available at https://cdr.ffiec.gov/.

[xiv] Alvin Lee, I’d Love to Change the World on A Space in Time (Columbia 1971).