Featured Article: It’s Not How You’re Buried: Estate Planning for Farmers and Ranchers by Dave K. Bagley II and Kelly C. Stevenson

In the movie “The Cowboys,” John Wayne’s character hires a group of schoolboys to help him on a 400-mile cattle drive. During the drive, they happen upon a skeleton in a shallow grave and the oldest boy, Cimarron, exclaims that the man wasn’t even buried in a proper grave. John Wayne’s character replies, “Well, it’s not how you’re buried. It’s how they remember ya.”

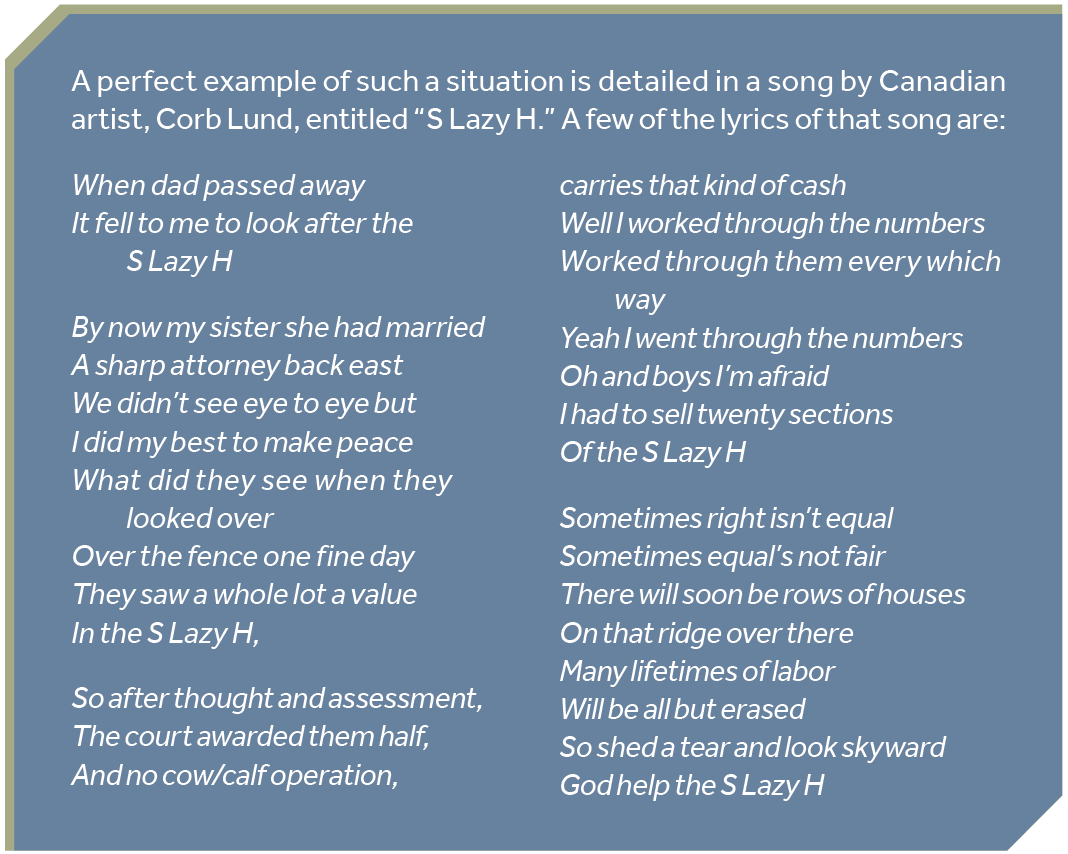

Idaho is full of farmers and ranchers who epitomize, in real life, the tough, self -reliant, independent ethos celebrated in the movies. Unfortunately, while family members left behind when a farmer or rancher dies may remember the deceased with love and pride, they may also face challenges distributing the deceased’s assets.

These challenges typically arise from one of two sources. One common frustration arises when a farmer or rancher dies without an estate plan at all. The second springs from having an estate plan not tailored to the client’s wishes.

If you are an estate planner who has dealt with agricultural clients, you have probably recognized the reluctance many farmers and ranchers have to think about, much less plan for, their own deaths. This reluctance probably stems from multiple sources. Farmers and ranchers tend to be strong and tough women and men.

Perhaps, thinking of their own deaths is subconsciously perceived as a weakness. Perhaps farmers and ranchers just don’t like or trust lawyers. Perhaps they deal with the difficult decision of how to structure an estate plan that provides for the children who “stayed” to assist with the management of the farm/ranch, and those children who “left” to undertake other life goals. Or perhaps they intuitively foresee difficult decisions that are deeply troubling in many cases and simply don’t want to think about it today, putting off these uncomfortable decisions to some future day.

The problem is that day may never come. Like it did for Wil Andersen, John Wayne’s character in “The Cowboys,” death sometimes arrives early and unexpectedly, before all plans could have been made. The Idaho Uniform Probate Code provides a default plan for decedents who die without a last will and testament or trust.[i] In some cases, that default plan is perfectly adequate. But, in many cases, it is not. For example, without a will naming a personal representative, family members (or others) must figure out who among them will serve in that capacity, potentially leading to acrimony and antagonism, delaying estate administration and increasing attorney fees.

A bigger problem arising under the Uniform Probate Code’s default plan relates to the distribution of assets. When a decedent dies without a will or trust, the default plan provides that 100 percent of the decedent’s share of community property goes to the surviving spouse, with 50 percent going to the decedent’s children.[ii] Under this circumstance, a surviving spouse is also entitled to other assets taken from the share otherwise going to the children.[iii] Particularly when the decedent had children from a prior marriage or relationship, these default distribution rules can lead to results significantly different than those likely preferred by the decedent. Similarly vexing problems can arise when a farmer or rancher remarries later in life without updating their estate plan or executing a prenuptial agreement.[iv]

Additionally, even if there is no dispute between a surviving spouse and a decedent’s children over the distribution of property, other problems can occur. The foremost problem, which will be addressed in more detail in the following, relates to situations in which only one child has been working the farm or ranch and feels it should go to them on their parents’ deaths. Under the Uniform Probate Code’s default plan, when the decedent leaves no surviving spouse, all of the decedent’s assets go to all of the children equally.[v] This could result in significant frustration and litigation, and to the loss of that child’s ability to continue to farm or ranch. Ultimately, it could also lead to the sale of the property outside of the family, which is often the last thing the decedent would have wanted.

What to do? Farmers and ranchers need to complete their estate planning. When representing a farmer or rancher on other matters, an attorney can take time to educate the client about the disadvantages of having no plan (or a plan that has not been updated) and encourage them to schedule an estate planning consultation.

Farmers and ranchers are often, in regular contact with their accountant and may respect their accountant’s recommendations as part of a long-term relationship. Accountants often serve like a general contractor for their clients—they may not perform all of the services that the client requires, but they can see and point out needs and provide recommendations and referrals. So, it is often the case that educating accountants on these matters can help them advise their farm and ranch clients of the need for estate planning.

Once a farmer or rancher has decided it is time to plan, the hard work really begins. Often one child in a family may work their entire lives on the farm or ranch, oftentimes in addition to their primary career, to keep the farm or ranch operating. The expectation (whether explicit or not) can be that they will solely inherit the farm or ranch when the parents are both deceased. This expectation gives rise to some common challenges.

One challenge is that sometimes the parents are not in agreement with each other as to whether the child should inherit the farm or ranch instead of all of the children inheriting equal shares. This must be handled carefully by estate planning counsel. In these situations, a spousal conflict waiver is advised, and the attorney needs to make sure that they are following all applicable ethical rules. Especially because an attorney may find that disagreement between the spouses makes dual representation untenable.

Additionally, spouses should be reminded that if the surviving spouse inherits the farm or ranch upon the deceased spouse’s death, the surviving spouse can, under most circumstances, alter some or all of the existing estate plan. There are ways to address that issue using trusts or other methods, the details of which are outside the scope of this article.[vi]

Another challenge can be the parents’ desire to be fair. This desire may manifest in parents wanting each child’s share of their estate to be equal in financial value. When clients have adequate assets in addition to the farm or ranch, this may be relatively easy. These types of assets could include cash, life insurance, retirement accounts, other businesses, and non-farm or non-ranch real property. In this situation, a client’s will or trust could provide that a valuation of the farm or ranch be conducted upon the death of the parents, that the farm or ranch go to the child who worked on it, and that the other assets be allocated to equalize inheritances among all of the children.

If a client does not have adequate non-farm or non-ranch assets to equalize inheritances, a difficult decision must be made. This usually results in one of three alternatives: the client leaving all of the assets to the children equally; requiring the inheriting child to “buy out” their siblings’ share of the farm or ranch over time; or leaving less to the children who do not farm or ranch. From an efficiency perspective, selling all of the assets and dividing the proceeds equally between all children is attractive.[vii] A buy-out plan can be tempting but the result is a change in the relationship between siblings.

Adding a business aspect to a familial relationship can set siblings up for conflict later if payments are late or if there is a default. Leaving all of the farm or ranch to only one of the children can be the fairest thing to do and can satisfy a client’s desire to keep the land in the family. But this can also result in frustration among the children who receive a smaller share of the estate and result in harm to sibling relationships. Children who receive less value often receive liquid assets or assets that can be quickly liquidated and, therefore, can immediately benefit financially whereas a beneficiary who inherits the farm or ranch can become land rich but cash poor.

Some parents leave farms or ranches that have significant development potential and could be worth much more as a subdivision. It is advisable to discuss this with clients and ask how they would feel if their child sold the farm or ranch rather than continuing to operate it. If this is a concern, parents may provide that if the farm or ranch were sold by the inheriting child within a certain amount of time, the proceeds be divided among all of the children. This can be a tempting approach but can lead to unintended consequences if not well-thought out. For example, it would be appropriate to account somehow for capital improvements made by the inheriting child. Of course, simplicity is generally the best approach, tending to be more robust and more likely to actually succeed than complicated plans.

“Like it did for Wil Andersen, John Wayne’s

character in “The Cowboys,” death sometimes

arrives early and unexpectedly, before

all plans could have been made.”

When leaving the farm or ranch to one child, it is vital to use precise and appropriate language. For example, leaving “the farm” or “the ranch” can lead to litigation over the definition of those terms. It is advisable to use legal descriptions when describing real property.[viii] Additionally, it is necessary to clarify the assets that must be left to that child to operate the farm or ranch. These could include, for example, all stock, crops, hay, equipment, proceeds from the sale of those items, contracts, and farm and ranch accounts.

Wills or trusts may leave farm real property to one child but remain silent regarding other items. This can result in equipment, crops, stock, and farm accounts going to all children equally though they may be necessary for the child inheriting the farm or ranch real property to operate. This is not only financially difficult for the child who was intended to continue operating the farm or ranch, but can lead to bitter fights between siblings. The will or trust must clarify with particularity which farm and ranch assets are to go to the child who inherits the land and which assets are to go to the other children.

Successfully navigating this approach requires confirmation of how assets are titled. Failure to confirm ownership and draft accordingly can lead to dire consequences. For example, a client’s will may leave the farmland to one child but, if the land is actually owned in an LLC, the client’s intentions may be frustrated. A client who leaves all “farm accounts” to one child could be setting up a fight with siblings if the farm account is commingled with the client’s personal account. Accomplishing the client’s goals requires a careful examination of asset ownership.

Another aspect of estate planning for farmers and ranchers involves federal estate tax. The estate tax is a tax on a decedent’s ability to transfer assets to beneficiaries at death and, primarily, is owed by the estate.[ix] For 2024, an exemption of $13.61 million dollars applies to each taxpayer.[x] In very general terms, this means that if the value of a decedent’s estate is less than $13.61 million at death, and the taxpayer has not reduced their exclusion amount by making large lifetime gifts, then no estate tax is owed. If the estate exceeds that amount, then, generally, the excess is taxed at 40 percent.

According to the USDA, less than one percent of farmers owed any federal estate tax in 2020.[xi] This may seem surprising given the increasingly high value of farms and ranches. However, two tax provisions have provided some relief to farm and ranch owners. “Portability” allows a surviving spouse to increase their individual estate tax exemption by the amount of their deceased spouse’s unused exemption.[xii] There are strict procedures and timelines to follow to take advantage of portability and the help of a tax professional is advised.

In addition to portability, the special use valuation rules help farmers and ranchers mitigate estate tax exposure. Under the special use valuation rules, a farm or ranch can be valued at its agricultural value rather than as a subdivision if certain criteria are met. Again, quickly retaining a tax advisor after a client’s death is important to take advantage of this rule.

“Successfully navigating this approach requires

confirmation of how assets are titled.

Failure to confirm ownership and draft

accordingly can lead to dire consequences.”

Currently, the estate tax exclusion is scheduled to be reduced by about half as of December 31, 2025, which could result in more farmers and ranchers facing estate tax liability. In addition to portability and the special use valuation rules, there are other approaches that can be taken to reduce or eliminate estate taxes. These can include family limited partnerships, irrevocable life insurance trusts, gifting, and other methods. For those clients who may have a taxable estate, reaching out to a tax advisor sooner rather than later is recommended.

Estate planning can dramatically affect our agricultural clients’ families and legacies. Helping preserve their heritage and avoid disputes between children can be exciting and fulfilling. Thankfully, there are many tools at our disposal to serve our clients and help our great Idaho ranching and farming families reach their goals.

Dave K. Bagley II teaches tax and business law at Idaho State University and is Of Counsel with Racine Olson, PLLP. He grew up wanting to be a cowboy until he realized how hard it was. Dave has ridden horses twice and dreams of someday owning a cowboy hat.

Kelly C. Stevenson is an attorney with Jones Williams Fuhrman & Gourley, P.A. She grew up raising and training horses, running cattle, and farming. She is the current chair of the Agricultural Law Section and its founder. Kelly represents agricultural clients in business formation, transactions, regulatory issues, estate planning, and litigation.

Endnotes:

[i] See Idaho Code §§ 15-2-101 et seq.

[ii] See Idaho Code §§ 15-2-102 and 15-2-103.

[iii] See Idaho Code §§ 15-4-401 et seq.

[iv] See Idaho Code § 15-2-301 et seq.

[v] See Idaho Code § 15-2-103.

[vi] Qualified terminable interest (QTIP) trusts are one way (among many) to provide an income stream for a surviving spouse while also addressing a spouse’s concern that the surviving spouse may revise an existing plan (at least with regard to the deceased spouse’s share of assets).

[vii] A child who wants to purchase the farm or ranch land or assets can still do so under this scenario. However, it can be financially prohibitive and can feel like a betrayal to the child who worked the farm or ranch for so long.

[viii] A title report can be helpful in determining whether the client owns the property that they think they own. Often there have been prior transfers of property or disputes with neighbors that can frustrate a plan if unknown.

[ix] See Internal Revenue Code Sections 2001 and 2002.

[x] See Internal Revenue Service Revenue Procedure 2023-34.

[xi] Less Than 1 Percent of Farm Estates Owed Federal Estate Taxes in 2020, Tia M. McDonald and Ron Durst, April 2, 2021 accessed at https://www.ers.usda.gov/amber-waves/2021/april/less-than-1-percent-of-farm-estates-owed-federal-estate-taxes-in-2020/ on July 8, 2024.

[xii] See Internal Revenue Code Section 2010 and Treasury Regulation 20.2010-2.